Single Platform vs. Fragmented Accounts | Elephants Inc.

Why SMEs are consolidating multiple financial tools into one platform in 2026 to cut costs and gain real-time visibility.

Why SMEs Are Replacing Fragmented Accounts With a Single Digital Financial Platform in 2026

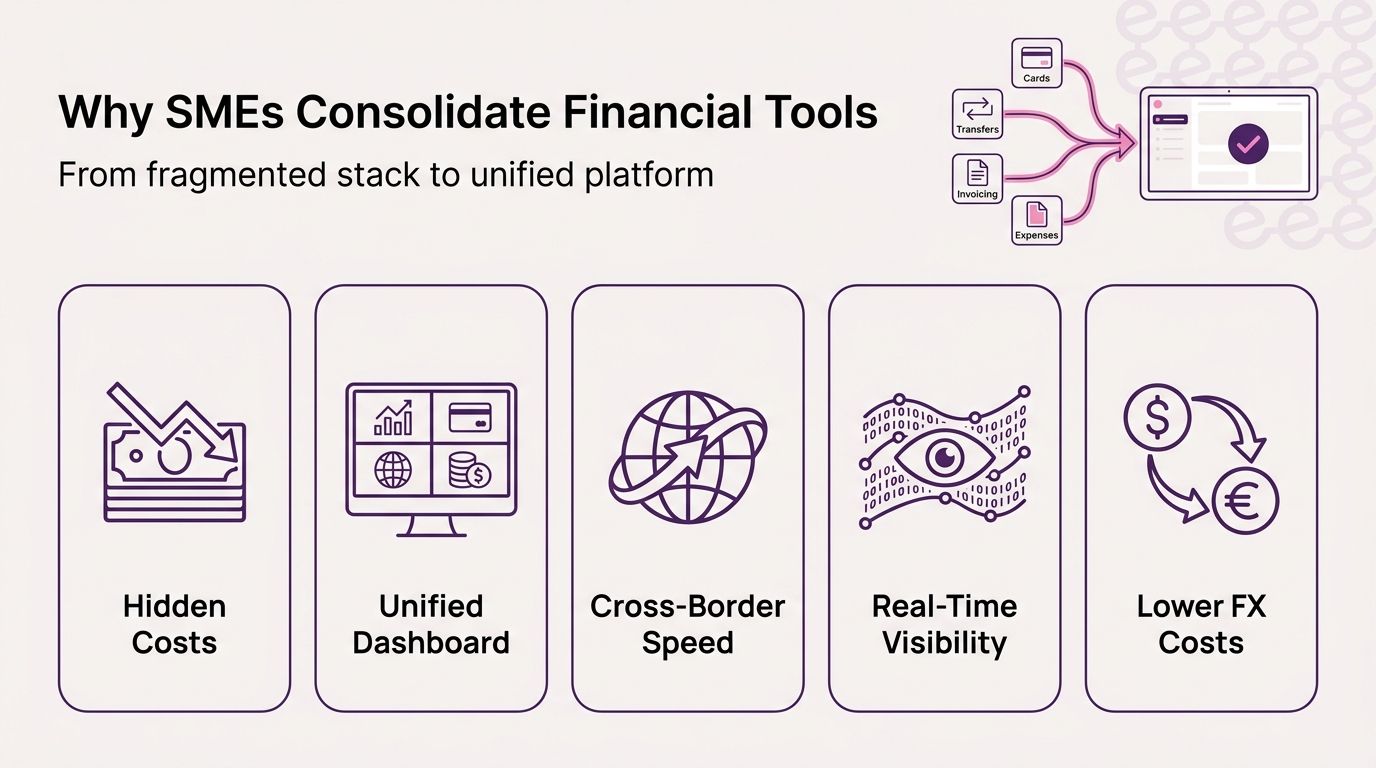

In 2026, the fastest-growing SMEs are not the ones with the most funding or the largest teams. They are the ones who figured out that running five separate tools for cards, transfers, invoicing, expense tracking, and foreign exchange is not just inconvenient, it is a measurable operational liability. The answer most of them are landing on is consolidation: a single digital financial platform that unifies all money movement under one dashboard, replacing the fragmented stack with unified visibility and control. This article explains exactly why that shift is happening, what it costs businesses to delay it, and what to look for in a platform that can actually deliver on the promise.

TL;DR

- Fragmented financial tools (multiple accounts, cards, spreadsheets, and FX providers) create hidden operational costs in time, fees, and reconciliation errors [glbank.com].

- SMEs globally face a significant gap in access to integrated financial infrastructure, which suppresses growth [worldbank.org].

- Consolidating onto one digital financial platform eliminates duplicate workflows, reduces FX costs, and gives finance teams real-time visibility across all spend and transfers [ledgerbee.com].

- The right platform covers cards, cross-border payments, invoicing, expense management, and AI-powered insights without requiring a traditional bank account.

- Elephants Inc. is a payments platform and digital wallet built specifically for this consolidated model, registered with FINTRAC as an MSB and with the Bank of Canada as a PSP.

About the Author: Elephants Inc. is a payments platform and digital wallet built to run a business, not just process payments. Serving SMEs and growing enterprises globally across 100+ currencies, Elephants Inc. combines cross-border transfers, smart cards, integrated invoicing, stablecoin support, and AI-powered financial insights in one unified platform.

What Does "Fragmented Financial Infrastructure" Actually Cost an SME?

Fragmentation is not just an inconvenience. It is a recurring, compounding burden on operational efficiency that most SMEs never fully measure.

When a business uses separate tools for each financial function, the costs stack up in at least three ways [glbank.com] [ledgerbee.com]:

Direct costs:

- Multiple platform subscription fees (e.g., separate invoicing tools, FX providers, expense software)

- Higher FX margins on international transfers because no single provider has visibility across the full payment volume

- Duplicate transaction fees when funds move between platforms before reaching a supplier or contractor

Indirect costs:

- Finance team hours spent on manual reconciliation across multiple statements and exports

- Delayed payment approvals because spend data lives in a different system from invoicing data

- Errors introduced when data is re-keyed between platforms

Strategic costs:

- No consolidated view of cash flow, which means decisions are made on incomplete information

- Inability to act quickly on supplier discounts or time-sensitive payments when the payment chain involves three systems

- Compliance risk from inconsistent record-keeping across disconnected accounts

Gary Chen, a business owner who uses Elephants Inc., reduced his FX and transfer fees by approximately 40% after consolidating, with global supplier payments clearing in minutes and over 10 admin hours saved per month on contractor payments. That is not an abstraction. It is a concrete return on switching.

Why Has Fragmentation Persisted for So Long?

Building on the cost picture above, a fair question is: if fragmentation is this expensive, why have SMEs tolerated it for so long?

The answer is structural. For most of the last decade, no single platform was genuinely capable of handling all financial functions at the quality level that specialists offered in each category. If you needed SWIFT transfers, you went to one provider. If you needed multi-currency invoicing, you used a dedicated invoicing tool. If you needed expense management, you added a third platform.

Small entrepreneurs have had to use several services to cover all their daily business needs simply because no single product existed that could do all of it well enough [theuxda.com]. The category of integrated digital financial platforms is relatively young, and the bar for moving all your money movement onto one platform is high.

What has changed in 2026 is the maturity of the category. Platforms now exist that combine payments, cards, FX, invoicing, and AI-powered analytics at a standard that matches or exceeds what category specialists offered individually three years ago [ebankit.com]. The consolidation thesis has moved from theory to practice.

What Should a Single Digital Financial Platform Actually Do for an SME?

A related but distinct question is what "consolidation" actually means in practice. Not every platform that calls itself unified is genuinely so.

A business expense management platform that replaces a fragmented stack needs to cover all four pillars of business money movement without gaps:

Hold

✓ What It Covers One wallet balance for both fiat + stablecoins

✕ Fragmented Setup Separate accounts for crypto and fiat

Send

✓ What It Covers Cross-border transfers in 100+ currencies

✕ Fragmented Setup Different providers per corridor

Collect

✓ What It Covers Named USD/EUR virtual accounts, integrated invoicing

✕ Fragmented Setup Invoicing tool disconnected from payment receipt

Spend

✓ What It Covers Business cards with spend controls, 0% FX on USD card spend

✕ Fragmented Setup Consumer cards or separate corporate card platform

When all four pillars live in one platform, the reconciliation problem largely disappears. Receipts auto-categorise. Invoices connect directly to payment status. Card spend and transfers appear in one statement. The finance function shifts from data assembly to decision-making.

How Does Fragmentation Specifically Hurt Cross-Border SMEs?

Cross-border operations amplify every fragmentation cost. A business paying suppliers in multiple currencies, collecting from clients in different jurisdictions, and managing a remote team across time zones is running the fragmentation problem at scale.

The global SME finance gap is estimated at US$5.7 trillion across emerging and developed markets, and a significant portion of that gap is not about credit availability but about the friction and cost of moving money efficiently across borders [worldbank.org]. When every international payment requires a separate workflow, a separate FX conversion, and a separate reconciliation step, the cumulative drag on growth is substantial [thunes.com].

Specific cross-border pain points that fragmentation makes worse:

- FX costs on card spend: Using a consumer card or a non-specialist corporate card for international purchases typically means paying the card network's standard FX margin plus the issuer's markup. A platform with 0% FX on USD card spend reduces fees compared to legacy banking alternatives.

- SWIFT delays: Businesses without named virtual accounts in the recipient's currency often wait days for settlement. Same-day clearing on supported corridors with local rail access improves supplier relationships and payment timing.

- Stablecoin friction: Web3-native businesses that operate partly in USDC or USDT have historically needed a separate account for that leg. Platforms that hold USDC, USDT, and fiat in the same wallet remove that friction entirely.

- Invoicing disconnected from FX: Sending an invoice in one tool and collecting the payment through a different FX provider means two reconciliation steps per transaction. Integrated invoicing solves this at the platform level.

What Does Consolidation Look Like in Practice? A Worked Example

Consider a product company with a remote team across three time zones. Before consolidation, their monthly financial stack looks like this:

- Corporate card platform (US-based, no multi-currency support): $45/month

- FX transfer provider for supplier payments: variable fees per transaction

- Invoicing tool (standalone): $25/month

- Expense management software: $30/month

- Manual spreadsheet reconciliation: approximately 12 hours/month of finance staff time

Total direct platform cost: approximately $100/month, plus variable FX fees. Total indirect cost: 12 hours of skilled labour per month, every month.

After moving to a single unified platform:

- One tiered plan covers cards, transfers, invoicing, and expense management

- Named USD and EUR virtual accounts allow clients to pay without correspondent bank routing

- 0% FX on USD card spend replaces the premium-rate consumer card

- Invoices are created, sent, and settled within the same platform, with auto-categorisation on receipt

- Stablecoin payments to contractors registered on the platform are sent in bulk, without a separate crypto account

The 12 monthly hours of reconciliation reduce significantly because the data is already unified. The FX savings compound with volume. And the finance team's attention shifts from assembling data to acting on it.

This is not a hypothetical. Mark Koh of VX Global reduced payment processing time from weeks to minutes after consolidating onto Elephants Inc., with corresponding cost savings from lower FX and transfer fees.

What Should SMEs Look for When Evaluating a Digital Financial Platform?

Building on the practical example above, here is a concrete checklist for evaluating whether a platform is genuinely unified or just a rebranded specialist tool:

- Regulatory standing: Is the platform registered with a recognised financial authority? Elephants Inc. is registered with FINTRAC as a Money Services Business and with the Bank of Canada as a Payment Service Provider under the Retail Payment Activities Act. This is the compliance anchor for trust.

- All four pillars in one dashboard: Does the platform genuinely cover hold, send, collect, and spend, or does it outsource one leg to a third party? -** Integrated invoicing vs. a separate tool**: Platforms like Keytom, Ramp, Brex, Wise, and Revolut do not integrate invoicing with their payments engine. Elephants Inc. does.

- Named virtual accounts without local presence: Can you open a USD account on SWIFT/ACH or an EUR account on SEPA without incorporating locally? Elephants Inc. offers both, subject to KYB. Competitors like KAST are US-only; Relopay and RedotPay offer none.

- Stablecoin support alongside fiat: If any part of your business touches crypto, the platform should hold USDC and USDT natively alongside fiat currencies.

- AI-powered insights, not just dashboards: Reactive dashboards show what happened. Ele, Elephants Inc.'s digital co-founder, monitors spend and flags anomalies via WhatsApp integration, giving you real-time financial analysis.

- Transparent, tiered fees: Flat-rate plans with named fees (Essential at $0/month, Explorer at $18/month, Elite at $38/month) make total cost of ownership predictable.

SMEs that migrate from fragmented tools to a unified platform gain more than efficiency. They gain unified visibility and control for every financial decision [ledgerbee.com].

Frequently Asked Questions

Is a digital financial platform the same as a bank account?

No. A digital financial platform is a payments platform and digital wallet that lets you hold funds, send and receive payments, manage cards, and issue invoices in one place. It is not offered by a bank. Elephants Inc. is a fintech payments platform, not a bank. Funds held are safeguarded for payment purposes, not insured.

Can SMEs use these platforms for cross-border payments without a local entity?

Yes. Named virtual USD accounts on SWIFT/ACH and EUR accounts on SEPA allow businesses to collect internationally without incorporating in each market, subject to KYB verification.

What is the difference between "bulk payments" and payroll?

Elephants Inc. facilitates bulk payment transfers only. It is not a licensed payroll or employer of record service. Customers retain full responsibility for their employment and tax obligations.

Are stablecoin payments genuinely useful for B2B transactions?

For businesses with contractors or suppliers who also hold stablecoin wallets, USDC and USDT payments clear faster than SWIFT on many corridors and carry lower fees. Bulk batch stablecoin payments to registered Elephants accounts are a specific B2B capability.

How do Ele Rewards work for business spend?

Card spend and transfers earn Elepoints at a rate of $1 USD to 1 Elepoint. Points are redeemable for flights at a 1:1 airline mile conversion. Hotels, VPNs, AI tools, and eSIMs are coming soon. Higher tier plans may provide improved conversion rates.

Is the platform available globally?

Yes. Elephants Inc. supports cross-border payments across 100+ currencies, and the card program is global. However, there are restrictions and not all products and services are available in every country or territory, and eligibility is subject to applicable regulatory and compliance requirements.

What happens to funds held on the platform if something goes wrong?

Funds held on the platform are safeguarded for payment purposes, not insured. Elephants Inc. is not a bank and does not hold customer funds in the banking sense.

Closing Thoughts

The case for consolidating onto a single digital financial platform is no longer theoretical. The platforms exist, the regulatory frameworks are in place, and the operational savings are measurable. SMEs that continue running fragmented stacks in 2026 are paying a recurring operational cost in fees, hours, and incomplete financial visibility, for no competitive advantage.

The shift is not about chasing the newest fintech product. It is about asking a straightforward question: how many platforms does it take to run your business finances today, and what would change if the answer were one?

If you are ready to consolidate your payments, cards, invoicing, and cross-border transfers into one platform, visit Elephants Inc. to learn more.

About Elephants Inc.

Elephants Inc. is a fintech payments platform registered in Canada as a Money Services Business and Payment Service Provider. Elephants Inc. is powered by Elephants Growth Tech Ltd who is registered with FINTRAC as an MSB and with the Bank of Canada as a PSP under the Retail Payment Activities Act. This enables Elephants to support foreign exchange, money transfer, virtual currency services, payment accounts, fund holding, and electronic fund transfers for end users.

Blog Release

Global Business Spend

Global Business SpendEle Rewards Explained: Business Card Points on Transfers

Earn airline miles on card spend and international transfers. The only global business rewards program with 1:1 conversion on both.

Crypto & Stablecoins

Crypto & StablecoinsWhy Your Business Should Accept Crypto in 2026 | Elephants Inc.

Discover why you should accept payments in crypto. Learn how stablecoins eliminate fees, stop fraud, and accelerate global growth with Elephants Inc.

Business Payments

Business PaymentsSmall Business Payment Systems: The Modernization Guide for 2026 | Elephants Inc.

Modernize your small business payment systems to reduce fees by 70%, automate invoicing, and earn rewards. A complete guide for global entrepreneurs.