Business Accounts for Web3 Founders 2026 | Elephants Inc.

Purpose-built digital platforms now let Web3 founders hold fiat and stablecoins, invoice globally, and pay teams-without traditional banks.

Web3 founders in 2026 face a structural problem that traditional banks were never designed to solve: running a business that moves money in both fiat and stablecoins, across multiple countries, without a local banking footprint. The short answer is that purpose-built digital financial platforms now fill this gap more effectively than banks or crypto exchanges alone. These platforms let you hold USDC, USDT, and fiat currencies in the same account, send to 100+ countries, collect payments on named USD or EUR accounts, and pay teams via stablecoin batch payments - all without a single bank relationship [bvnk.com][ventureburn.com].

TL;DR

- Traditional banks cannot handle stablecoins; most crypto-card products cannot handle invoicing or bulk payments - Web3 founders need both.

- Digital financial platforms registered as Money Services Businesses (MSBs) and Payment Service Providers (PSPs) are the compliant middle ground in 2026.

- Key capabilities to prioritise: unified fiat + stablecoin holding, named virtual accounts (SWIFT/ACH/SEPA), integrated invoicing, and batch payments via stablecoin rails.

- Fee structures vary sharply: 0% FX on USD card spend (Elephants Inc.) versus 1% or higher at most alternatives.

- Regulatory registration matters: FINTRAC registration as a Money Services Business (MSB) and Bank of Canada registration as a Payment Service Provider (PSP) under the Retail Payment Activities Act signal a verifiable compliance anchor in an otherwise fragmented market.

About the Author: This guide is produced by Elephants Inc., a FINTRAC-registered Money Services Business and Payment Service Provider serving Web3 founders and globally-operating SMEs across 100+ countries. Elephants' direct experience operating fiat and stablecoin infrastructure for companies including Cryptomind, Chintai, and Coinranking informs every recommendation in this article.

Why can't Web3 founders just use a regular business bank account?

Traditional banks were built for a world where money is always fiat, always domestic, and always slow. Web3 businesses break every one of those assumptions from day one. Most conventional business accounts will freeze or close the moment stablecoin activity is detected, cannot receive USDC or USDT at all, and treat international wire transfers as a compliance risk rather than a routine operation [bvnk.com].

The practical result is that founders cobble together three to five separate tools: a crypto exchange for stablecoin conversion, a payment processor for invoices, a card provider for SaaS subscriptions, and a remittance service for overseas contractors. Each tool carries its own KYC queue, fee structure, and reconciliation headache. The average Web3 startup wastes more than ten admin hours per month just keeping these systems in sync.

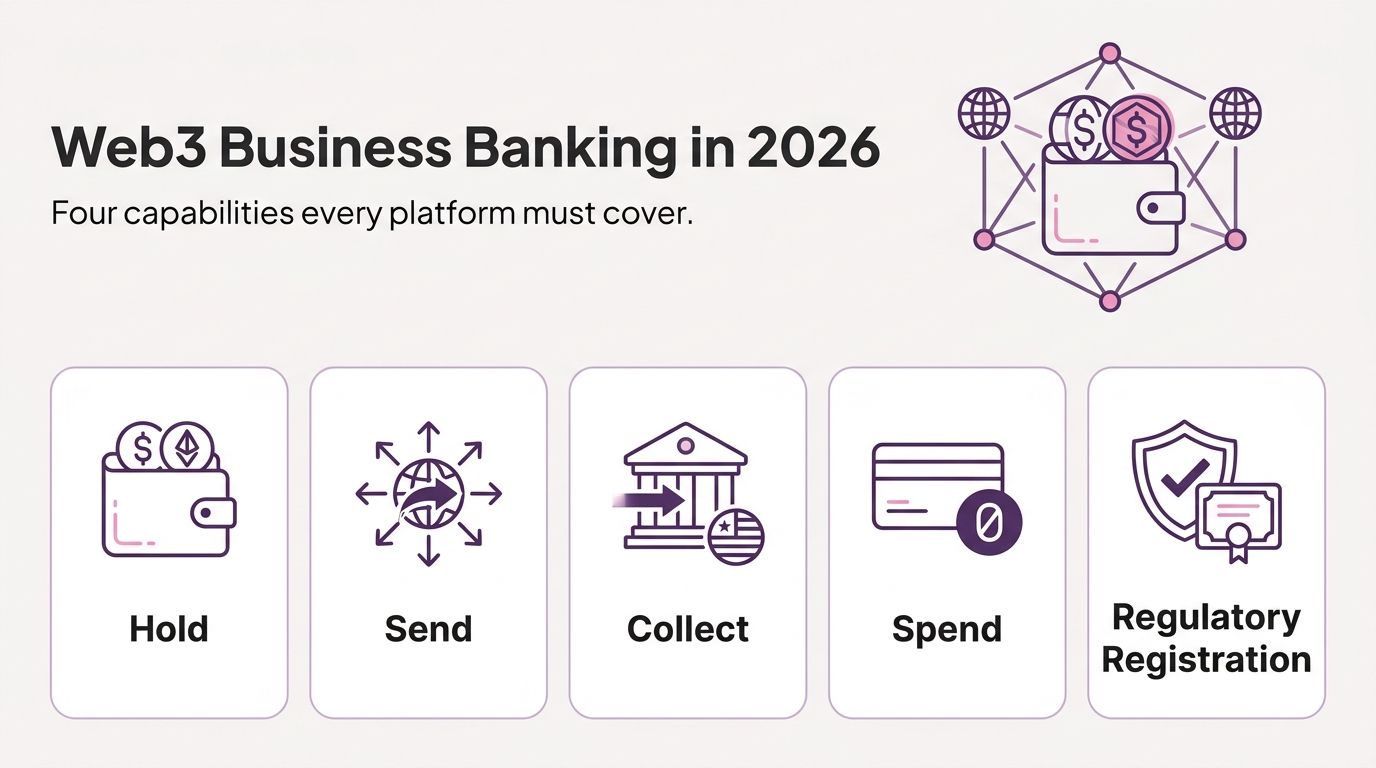

What should a business account for a Web3 company actually do in 2026?

The harder question is what a purpose-fit solution looks like. A useful framework is four core capabilities: Hold, Send, Collect, and Spend.

Hold

✓ What it means for Web3 founders

Store USDC, USDT, and fiat in one account with minimal conversion costs.

✓ Why it matters

Avoids forced liquidation at unfavourable exchange rates.

Send

✓ What it means for Web3 founders

Pay contractors and suppliers in 100+ currencies across supported payment corridors.

✓ Why it matters

Eliminates multi-day delays and layered correspondent banking fees.

Collect

✓ What it means for Web3 founders

Named USD/EUR virtual accounts on SWIFT, ACH, and SEPA without needing a local entity.

✓ Why it matters

Clients can pay you as if you were a local business in their country.

Spend

✓ What it means for Web3 founders

Visa cards with 0% FX on USD card spend, configurable team spending limits, and real-time expense tracking.

✓ Why it matters

Removes FX costs on everyday SaaS subscriptions and business spending paid in USD.

Any platform that covers all four in a single dashboard with integrated invoicing is a stronger fit than stitching together separate tools [trustlinq.com].

How do digital financial platforms compare to crypto-card-only solutions?

A related but distinct question is whether a crypto-linked debit card alone solves the problem. It does not, for one structural reason: crypto cards handle spend, but Web3 businesses also need to receive money professionally (invoicing), pay teams at scale (batch payments), and hold multiple currencies without converting to a single base currency.

What does regulatory registration actually mean for my business?

Stepping back from the product comparison, a separate concern is compliance risk. In 2026, regulators across the US (FIT21), EU (MiCA), and Canada (FINTRAC) are tightening oversight of digital currency businesses [crassula.io]. Founders who use platforms without clear regulatory anchors carry that counterparty risk directly.

Elephants Inc. is powered by Elephants Growth Tech Ltd, registered with FINTRAC as a Money Services Business (MSB) and with the Bank of Canada as a Payment Service Provider (PSP) under the Retail Payment Activities Act (RPAA). This is a concrete, verifiable compliance standard. It requires the platform to maintain anti-money laundering programs, report suspicious transactions, and meet ongoing regulatory obligations. For founders building in the Web3 space, where investors and enterprise clients increasingly run counterparty due diligence, choosing a FINTRAC-registered MSB and Bank of Canada PSP is a defensible answer in any compliance conversation.

How should a Web3 founder evaluate stablecoin bulk payment options?

Building on the compliance point above, stablecoin bulk payments are where most platforms fall short in practice. Paying contractors in USDC or USDT requires audit trails, role-based approval controls, and the ability to send to multiple recipients in a single operation without manual wallet entry for each [trustlinq.com][ventureburn.com].

Elephants facilitates bulk payment transfers only and is not a licensed payroll or employer of record service. Customers retain full responsibility for their employment and tax obligations. Key criteria for evaluating stablecoin bulk payment infrastructure:

- Can you send to multiple recipients in a single batch, not one at a time?

- Are transaction records exportable for accounting and tax purposes? [irs.gov]

- Does the platform support both USDC and USDT, or only one?

- Are recipients required to hold accounts on the same platform, or can they receive to external wallets?

- Is there a clear fee structure per batch, or are fees buried in conversion spreads?

Frequently Asked Questions

-

Can a Web3 business legally hold stablecoins in a business account in 2026? Yes, on platforms registered as Money Services Businesses with digital currency authorisation. Regulatory frameworks like FINTRAC in Canada and MiCA in the EU now provide clear compliance pathways for businesses holding USDC and USDT [crassula.io].

-

Do I need a local company to open a named USD or EUR account? No, on platforms that offer virtual USD accounts on SWIFT/ACH and EUR accounts on SEPA, you can collect in those currencies without local presence, subject to KYB verification.

-

How are stablecoin transactions taxed for businesses? Tax treatment of digital assets varies by jurisdiction. In the US, the IRS treats digital asset transactions as reportable events [irs.gov]. Always consult a qualified tax adviser for your specific structure.

-

What is the difference between a crypto card and a business digital account? A crypto card handles spend only. A digital account also covers receiving (invoicing, named accounts), holding multiple currencies, sending cross-border payments, and managing team expenses in one place [bvnk.com][ventureburn.com].

-

Is 0% FX on USD card spend possible without hidden fees? Yes, when a platform operates at sufficient volume and uses transparent tiered pricing. Elephants Inc. charges 0% FX on USD card spend across all plan tiers,

-

How do I pay international contractors without a traditional wire transfer? Digital financial platforms with stablecoin batch payments and 100+ currency local rails let you pay contractors in their preferred currency or stablecoin on supported corridors, [trustlinq.com]. Elephants facilitates bulk payment transfers only and is not a licensed payroll or employer of record service. Customers retain full responsibility for their employment and tax obligations.

-

What should I look for in an AI financial assistant for my Web3 business? Prioritise real-time data access, spend categorisation, cash flow alerts, and natural-language querying. The assistant should pull from live transaction data, not periodic syncs.

About Elephants Inc.

Elephants Inc. is a non-bank digital financial platform for the AI era - not a bank, a smarter way to operate. Powered by Elephants Growth Tech Ltd, registered with FINTRAC as a Money Services Business (MSB) and with the Bank of Canada as a Payment Service Provider (PSP) under the Retail Payment Activities Act, Elephants serves Web3 founders and globally-operating businesses across 100+ countries. The platform combines USDC/USDT stablecoin support, named USD and EUR virtual accounts, integrated invoicing, stablecoin batch payments, 0% FX on USD card spend via Visa business cards, and an AI co-founder (Ele) accessible via WhatsApp - replacing the fragmented stack of cards, accounts, and spreadsheets with a single source of truth for business spend and transfers. Ready to run your Web3 business finances without the fragmentation?

Explore what Elephants Inc. can do for your team at elephants.inc

References

- How to accept cryptocurrency payments as a business (2026 Guide) | BVNK Blog (bvnk.com)

- Use Crypto to Buy Anything in 2026 | TrustLinq (trustlinq.com)

- How to Accept Crypto Payments: A 2026 Guide for Businesses (ventureburn.com)

- Cryptocurrency Exchange 2026 | CEX vs DEX, MiCA, Launch Playbook | Crassula (crassula.io)

- Digital assets | Internal Revenue Service (www.irs.gov)

Elephants Inc. is a fintech payments platform registered in Canada as a Money Services Business and Payment Service Provider. Elephants Inc. is powered by Elephants Growth Tech Ltd who is registered with FINTRAC as an MSB and with the Bank of Canada as a PSP under the Retail Payment Activities Act. This enables Elephants to support foreign exchange, money transfer, virtual currency services, payment accounts, fund holding, and electronic fund transfers for end users.

Blog Release

Global Business Spend

Global Business SpendEle Rewards Explained: Business Card Points on Transfers

Earn airline miles on card spend and international transfers. The only global business rewards program with 1:1 conversion on both.

Crypto & Stablecoins

Crypto & StablecoinsWhy Your Business Should Accept Crypto in 2026 | Elephants Inc.

Discover why you should accept payments in crypto. Learn how stablecoins eliminate fees, stop fraud, and accelerate global growth with Elephants Inc.

Business Payments

Business PaymentsSmall Business Payment Systems: The Modernization Guide for 2026 | Elephants Inc.

Modernize your small business payment systems to reduce fees by 70%, automate invoicing, and earn rewards. A complete guide for global entrepreneurs.